Edited and updated remarks presented to the Economic Development Australia, National Economic Development Conference 2014, Doubletree Hilton Hotel, Darwin, Wednesday 29 October 2014

Some framing issues for future Australia

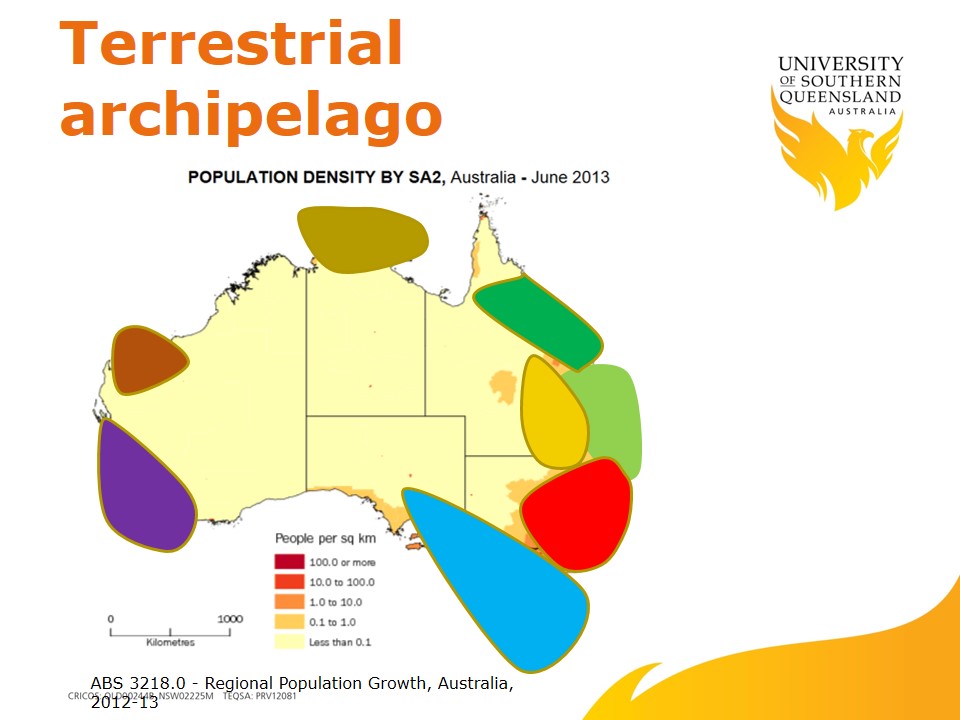

Will we continue to develop as a terrestrial archipelago?

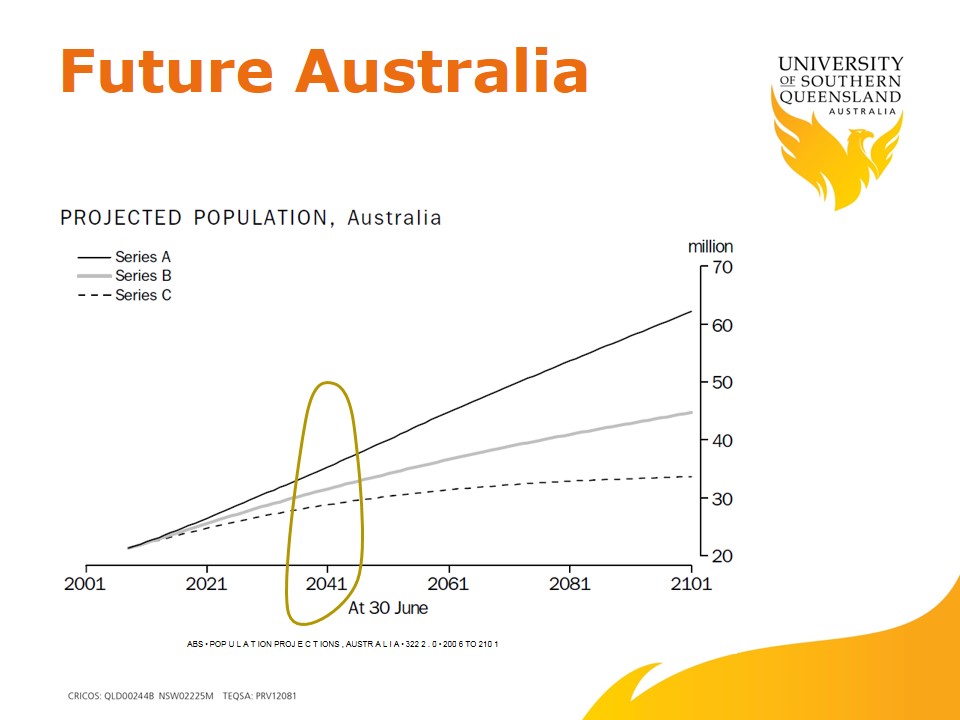

Mid range population projections for Australia predict a population of around 37 million by 2040. If past and present settlement practices are any indication, those 37 million will not be distributed to all parts of the continent but will cluster around the major metropolitan and peri-urban centres on the coast.

I was reminded some years ago when flying across to Broome from Brisbane that from the air the dune patterns of arid inland Australia looked remarkably like the vast ocean floor it was a hundred million years ago.

Flying across that vast expanse from coast to coast, with a re-fuelling stop in Alice Springs, it struck me that modern European Australia is a ‘terrestrial archipelago’ of human habitation clinging to the seashore of an island continent.

Less than 0.1 person per square kilometre is the population density of most of this vast continent.

David Malouf called the Australians of the modern era a “sea-dreaming people” settled by “little-islanders” from Britain. He wondered had Australia been settled by Russians instead would they have “learned to live more easily with distance and space?”

If people are moving anywhere in Australia right now, they are moving to the cities or from the metropolitan capitals to inner regional centres nearby.

So people in Bendigo or Ballarat are right in the middle of modern regional development in Australia, but those living in northern Australia or western Queensland see a very different world of, rural decline and struggling near dead small towns.

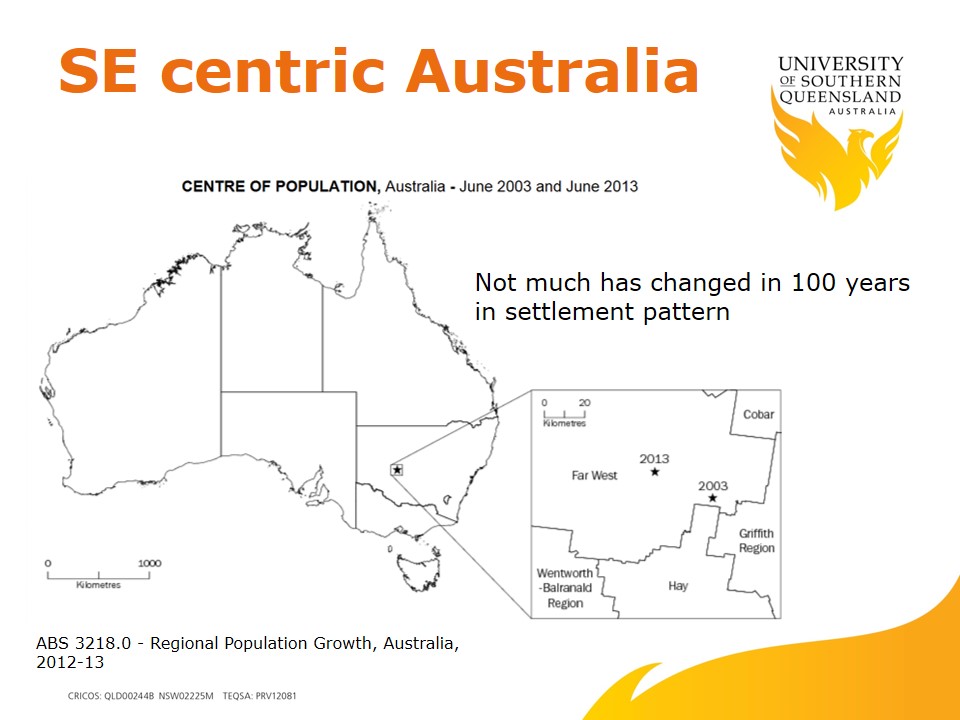

Over the past 100 years the population centricity of European Australia has not changed very much at all – it was and remains SE centric.

Over the past 100 years the population centricity of European Australia has not changed very much at all – it was and remains SE centric.

To the dismay of those living in Perth, over the past decade the epicentre of the Australian population has moved about 20 kilometres west in the Riverina district of southern NSW.

Much of our broad land remains the province of FIFO and DIDO workers – the regions accounting for 60% of Australian exports, 80% of our export income, and next to nothing in population and communities.

Can we expect much different in the future? Probably not. Our national infrastructure deficit prohibits the intensity of regional development as has occurred say in the United States.

Northern development?

Attending a regional development conference recently in Albury, the notion of a northern Australian strategy which might see it rival agricultural output in southern states seemed far fetched.

But to NT’s Chief minister Adam Giles and other northerners the idea of an agricultural revolution in the north is no fantasy.

According to the New Scientist the region north of the Tropic of Capricorn receives a lot of rain, a quadrillion litres in fact (that’s a million billion) and has more than 1.7 million hectares that could potentially be irrigated.

Northern Australia also contains 25% of Earth’s savannah and experiences rapid evaporation – and is home to a significant proportion of Australia’s indigenous people.

I think Brian Haratsis is right in saying that the defence sector – along with energy – is more likely to be the major economy in this part of the world in the years ahead.

The Top End, as I have said, abuts a region that straddles one of the key geo-strategic fault-lines where capacity to project military power might become necessary.

As to any farm revolution here, it’s likely to be in tropical crops. I hear much talk of sugar cane for example, around the Gulf in northern Queensland.

A colleague in CSIRO told me that because the northern output is more likely to be “salad” rather than protein, the net increase in calorific value for Australian agriculture could be as little as 1%.

Between 1980 and 2005 more than 90 abattoirs closed in regional Australia, in part because of poor transport infrastructure, remoteness from major markets and ports, and costly industrial arrangements. These barriers to rural development have not been fixed.

Most recently the ANZ Bank has come out with a report, “Molehill to Mountain: agriculture in northern Australia”, that found that the idea of investing in large irrigated broad acre tracts of the north would likely result in unprofitable white elephant cropping projects.

The ANZ report points to the desirability of investing improved infrastructure in the existing live cattle and beef industries as a better pathway – a view shared by the Northern Territory Farmers Association.

More generally, when we talk about the future of remote regional Australia, I think Barry Traills from the Pew Foundation said it well when he said we had to “get beyond the mythology” of the Outback.

Frankly, European communities and ways and means are never going to cut it sustainably in much of remote Australia – the climate is too harsh, the land too old, and the distances and isolation too great.

Would it not be better if this vast expanse, nearly 70% of the continent with just 5% of the population was left to be preserved in its essential indigenous and ecological character – a major international tourism destination, a platform for various initiatives in international education and research?

We should be working with Aboriginal Australians to make sure that the Outback becomes a world famous beacon as one of the great reserves of the global biosphere and of indigenous language and culture.

Warmer Australia

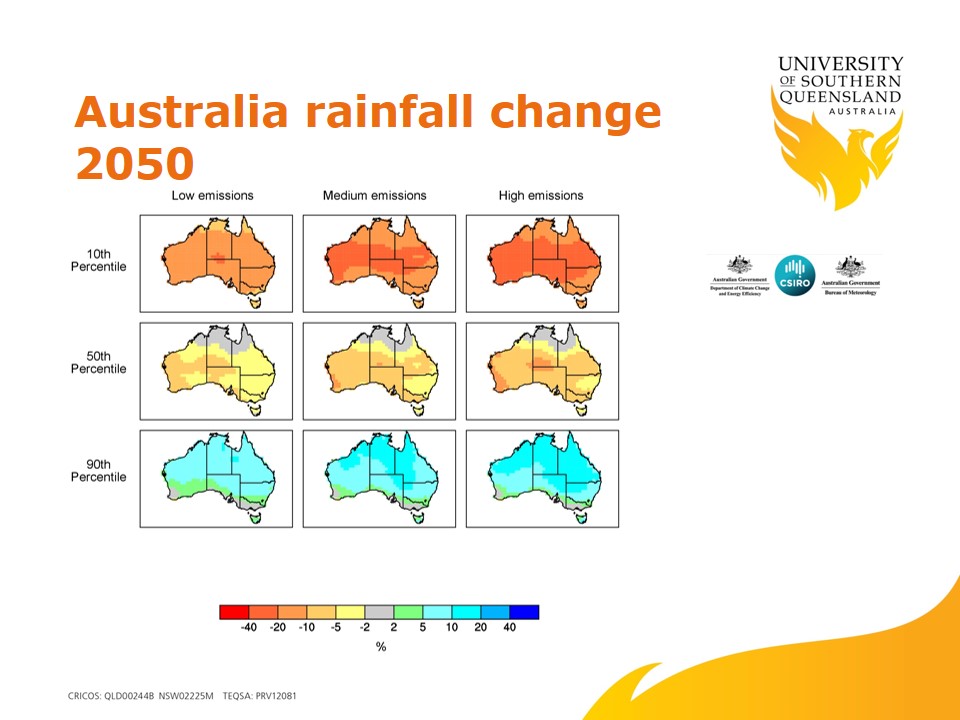

As I said earlier, in much of regional Australia global warming is going to present more immediately and acutely.

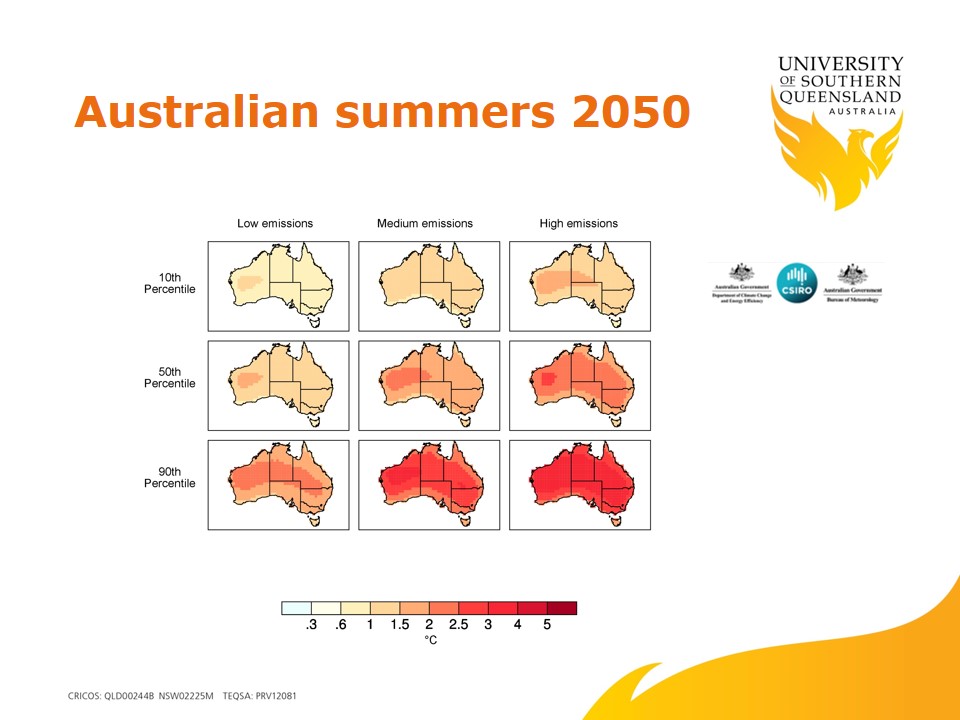

By the 2050s inland areas already evidencing climate impacts could be as much as 2°C warmer and that means a far more volatile and variable climate than is already experienced in those districts – in temperature and rainfall terms.

This has real implications for Australian agriculture and particularly the pastoral industry. As my USQ colleague, Professor Roger Stone, routinely points out, Australia already has the most variable climate of any country on Earth.

Our pastoral industry in northern and central Australia spans regions which are the most climate variable in the most climate variable country. Talk about dealing with double jeopardy.

Climate change means Australia faces risks accentuated by its comparatively strong carbon dependence.

The economic quandary for Australia arising from climate change generally will be how to efficiently de-carbonise its economy as global initiatives are made to mitigate human causes of climate change while accelerating the adaptive capacity of a host of very different economies.

In the absence of a viable clean coal technology, for example, thermal coal exporting states could find themselves with a product no one wants to buy – with consequent economic dislocation in the mining regions and impacts to government revenues.

This intermediate prospect makes highly questionable if not irrational the Queensland Government’s commitment of $300 million of taxpayer’s money to providing rail and port infrastructure to the proposed Galilee coal mining developments.

Changing society risks and opportunities

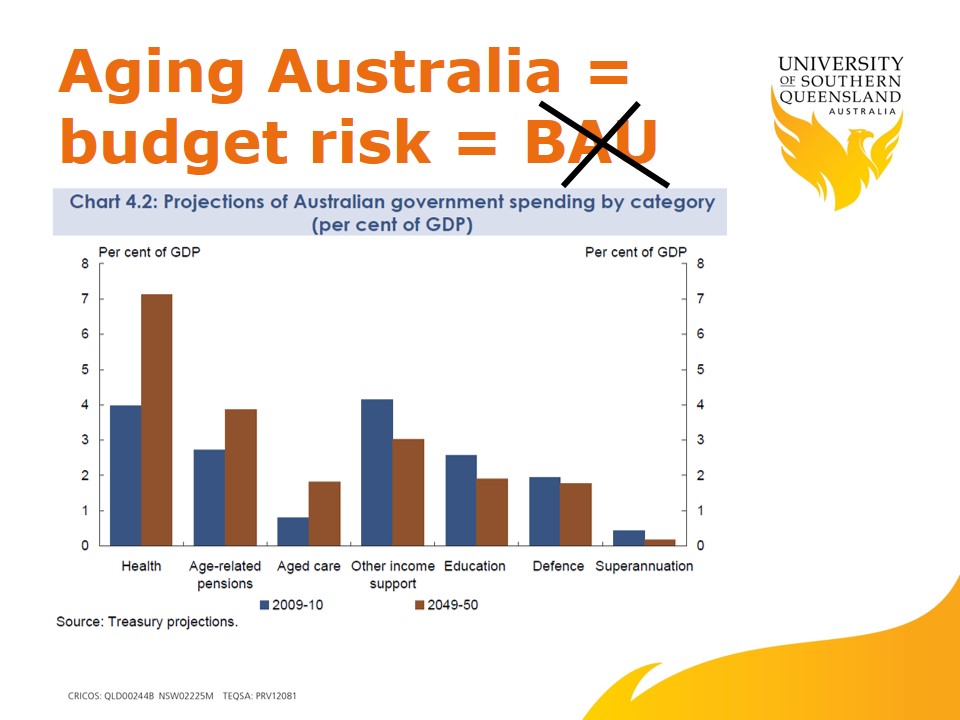

On another tack – that of government and the costs associated with changing Australian demography into the future, the budget risk associated with spiralling health expenditure was mentioned by Brian in his talk.

Treasury projections show by 2050 expenditure on health, aged care and pensions outstripping all other expenditure combined. It’s a prospect we cannot afford, particularly as we will have fewer taxpayers relative to the over 65 population.

But the aging population trend also presents major economic and social opportunities in providing the goods and services that enable people to remain self-reliant, productive, connected, mobile, and community involved.

And not to put too fine a point on it, what is the point of extending life expectancy if we fail to solve issues like Alzheimer’s and aged dementias which rob patients and their families of quality of life.

Simply because of the numbers involved and the size of the market globally, Quality of Aged Life industries, technologies and services will be on the rise and the opportunities will not be just in the domestic market.

By 2030 China will have 250 million people over the age of 65 – the economic development opportunities associated with aging will be global in magnitude.

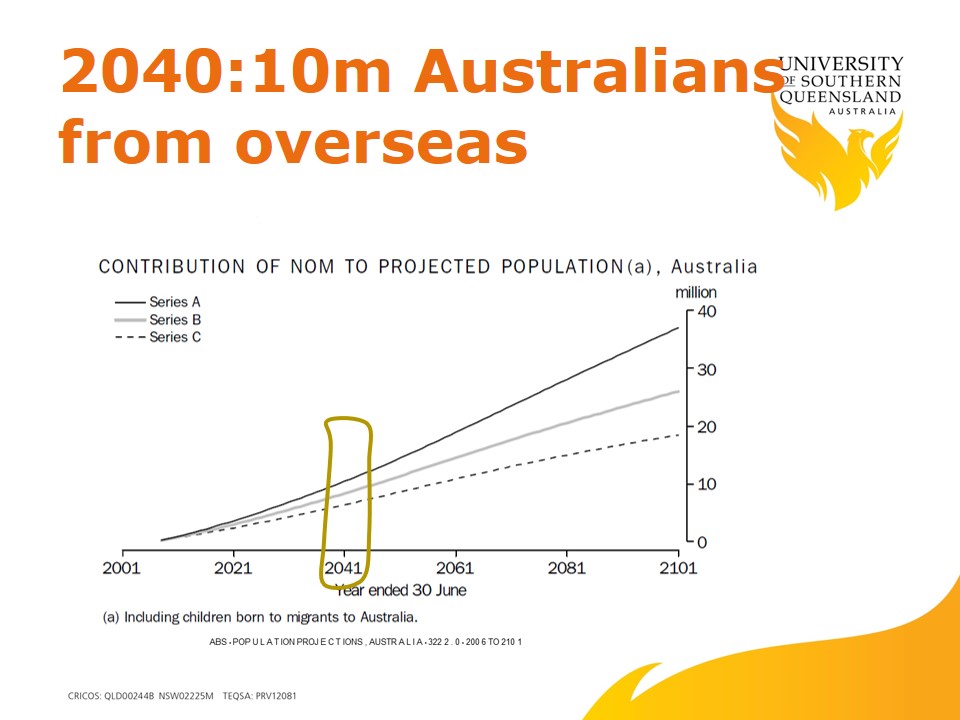

Australian society in 2040 will also be more racially and ethnically diverse than it is today with upwards of 10 million Australians by then being born overseas. We are already a polyglot country of immigrants and this defining characteristic is set to continue.

Hopefully these new arrivals will bring with them some of the skills and capacities to build a vital competitive country relevant to the middle and latter half of the century. Waves of immigration have contributed to the broadening and diversity of our country making Australia much more “anti-fragile” than it would otherwise have been as an Anglo antipodean outpost.

Australia in Asia – success means more than trade

The increasing Asian proportion of the Australian population is likely to provide a human bridge back to the burgeoning economies to our north about which there is a bipartisan consensus as to their importance to Australia’s future.

Central to the Australian expectation about Asia is the continued growth and stability of its core economies: China, Japan, South Korea, and to a lesser extent India. The ASEAN archipelago constitutes an essential regional portal to Asia for Australia and increasingly we will have to create a more engaged partnership with Indonesia.

The economic focus is on the rising Asian middle class – in itself a product of the economic transformation of the east Asian region and which will involve increasingly the growth of consumer demand inside their own economies (instead of infrastructure investment as has been the case).

Australia is a key external stakeholder in that transition. Close to two thirds of our exports are covered by the FTAs recently signed with Japan, South Korea and China.

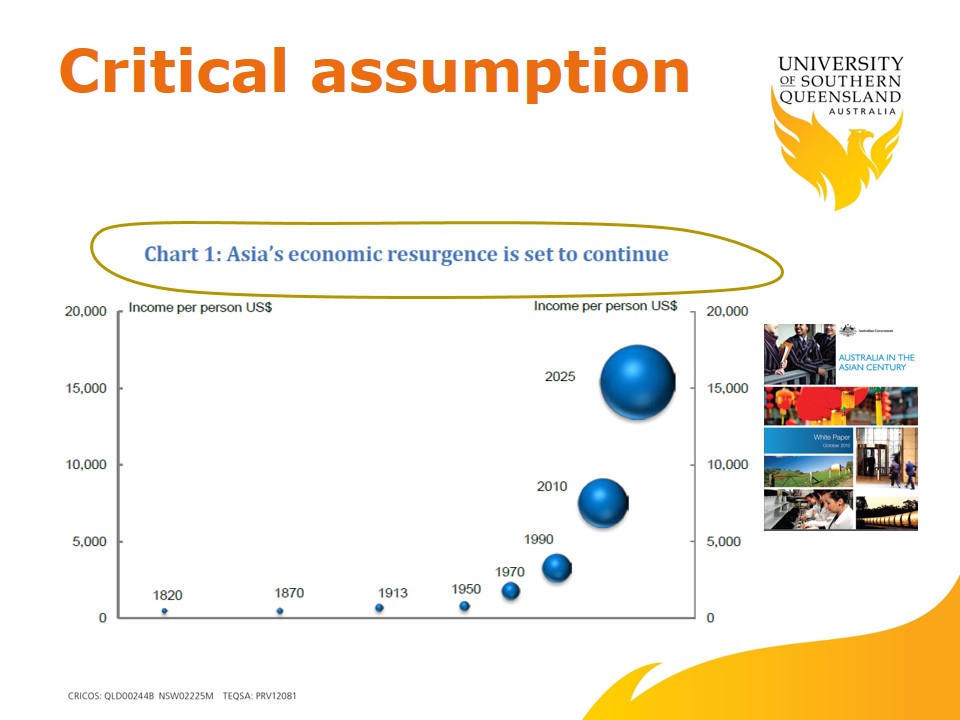

Treasury projections hold that the exponential growth in Asian per capita incomes will extend to 2025 to approximately $US 15,000 – more than twice what they are now.

Again this is all trend analysis and must be considered accordingly.

There are good reasons not to share the general confidence of a future so “exponentially” simplistic.

Socio-economic unrest afflicts western and semi-autonomous regions within China particularly. The core question for the world really is whether China can mature politically as well as economically over the coming quarter century without a cataclysmic upheaval.

And no country important to Australia is immune to the risks of an increasingly inter-connected global economy, including key Asian economies. Trade in the Asian region has grown by 500% since 2000 meaning no one is master of their own destiny.

As far as India is concerned, its history, culture and enormous urban/rural divide give its economy a sclerotic quality which hinders the pace, character, and extent of its development.

Professor Henry Ergas points out that India’s per capita income is only half that of China’s, and to catch up “India’s growth in per capital income must go from its 4% average since 1980 to 6%”.

For this to happen, the new reformist Prime Minister Narendra Modi will have to overcome what Ergas rightly described as “pervasive economic distortions” across the country.

It’s why I would not hold my breath waiting for the Galilee coal basin to be developed in Queensland, notwithstanding the Queensland Government approving five new coal mines there.

More concerning, frankly, is that Australia needs China to keep growing at more than 4% for us to avoid recession. How feasible is that over the intermediate term?

The growth of its middle class by a further 850 million people (or six Japans) by 2030 – assuming no catastrophic political, ecological or economic upheaval makes it at best an even bet.

China is now the market for 38% of Australian exports. As Deloitte Access Economics reported recently: “If something goes wrong in China than its batten-down-the-hatches time in Australia”.

The recently signed FTA with China will make 85% of our exports tariff free, expanding to 95% after four years and integrating us even more closely with the fate of the Asian behemoth.

Avoiding the critical path dependence folly

Critical path dependence, that is Australian dependence on Chinese economic growth, is a fundamental risk we must take closer account of to create diverse options that protect us from a possible implosion of the Chinese economic miracle.

Annual Australian exports to China hit a high mark of $100 billion in the year to April 2014 but with falling commodities prices export values there have been falling ever since.

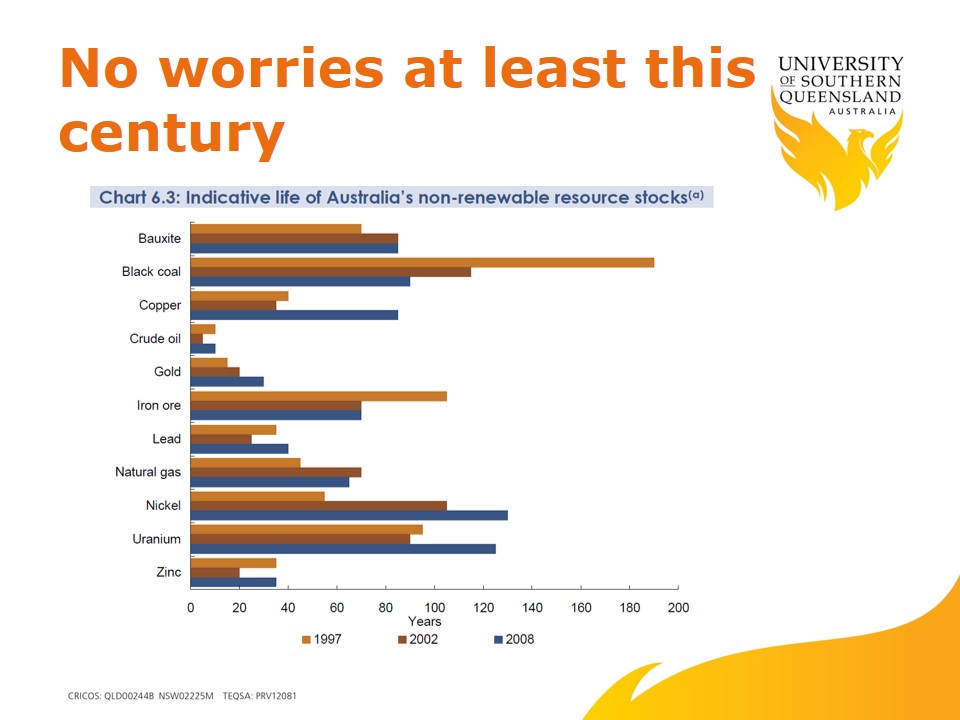

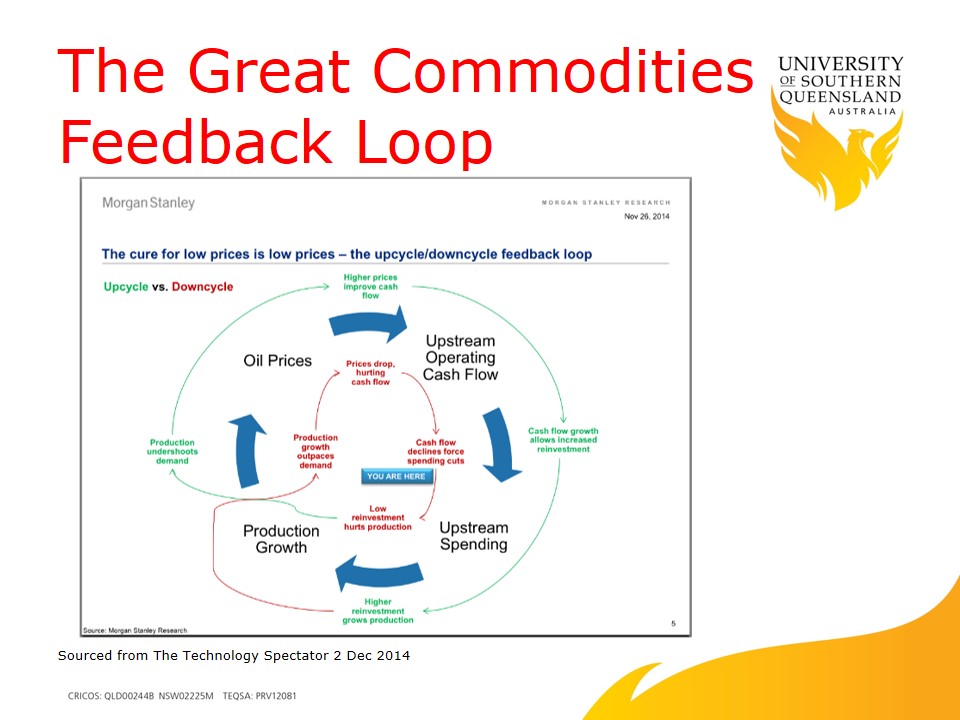

The indicative life of Australia’s non-renewable resources indicates that we could get through this century providing our raw materials to other countries – but sometime off into the future we will run out and what then?

And in the meantime are we condemned as a nation to alternating booms and busts reflective of the commodities cycle until we run out of resources to export?

Orthodox government thinking seems to indicate this will be the case. The Bureau of Resources and Energy Economics (BREE) points to the stock of resources investment dropping by $150 billion out to 2019, but it adds reassuringly “there remains the potential for further investment in the future….. when market conditions permit”.

The Big Four Banks evidently also think so. They show no signs of limiting their exposure to the volatility that comes with commodities business. Since January 2008, stock market environmental activist Market Forces reports, major Australian banks have accounted for about $19 billion of the $80 billion loaned to the resources sector.

Rather than wait for the country to run off a cliff, a prudential approach to national development suggests that Australia diversify its economy through innovation and clever technological and services industries that will have a globally competitive capacity – that is having the ability to contribute to the globally linked supply chains feeding into major markets.

We can be a serious food player, for example, but only with the production limits of a hot and largely arid continent needing massive amounts of patient investment. For that to happen we will have to be more accepting of foreign investment starting with China which has nearly 20% of the global population but just 10% of its arable land – relentlessly threatened by urban industrialisation and pollution.

Currently, 95% of the 134,000 farms in Australia are family owned and rely on private equity and bank debt to finance their operations. The Big Four Australian banks have a $107 billion exposure to the agricultural sector. But as ANZ/Port Jackson Partners revealed back in 2012, there is an annual $9 billion investment shortfall from the levels needed for Australia to make the most of the burgeoning Asian food market.

Investments by the likes of resources tycoons Andrew “Twiggy” Forrest and Gina Reinhardt point to the opportunity in agriculture, but Australian financiers are not rushing to become farm investors.

If the funding is to occur it will have to come from somewhere else.

Trouble is a majority of farmers and three in five Australians oppose foreign ownership of our farmlands, even though according to the ABS only 12% of farmland is owned by overseas interests. But as Barnaby Joyce reminds us, this is an area two and a half times the size of Victoria – and that’s enough to prick the hackles of many voters uninterested in finding a way forward for Australian agriculture.

More fundamentally, as former Prime Minister Bob Hawke has cautioned, if we are to exploit the opportunities of a rising Asia, especially a rising China, “we have to abandon the idea that the relationship can only be economic”.

Are we up to an innovative future?

The $200 billion Australian LNG industry soon to be the largest LNG exporter in the world is virtually an overnight phenomenon driven by the broader changes happening in the global energy mix. Arguably most of the technology to develop the LNG industry has had to be imported and draws more from Houston and Aberdeen than it does from Perth or Brisbane.

A key question for Australia going forward is how to we capture and commercialise the experience of developing our massive reserves of natural resources? How do we build hi-tech services and infrastructure industries off the back of these developments?

CEO of the Australian Industry Group, Innes Willcox, drew out Australia’s economic challenges for the coming decade very clearly when he said recently:

“Like any good business Australia needs to focus on its competitive strengths, intellectual capital and skills base to value add in resources, agriculture and manufacturing to give us the balanced sustainable economy we need with a distinctive competitive edge.

“There is a role for government to build the infrastructure and skills base and reduce the taxation, regulatory and cost burdens to allow business to invest and to book the new globally competitive economy we need, Australia maybe an island, but we can’t afford to be an island economy”.

In framing how it believed Australia should address the future, the release recently by the Federal Government of its Industry Innovation and Competitiveness Agenda drew heavily on input from the Business Council of Australia.

And from an “anti-fragile” perspective that is its greatest weakness. It is a plan for a corporate Australia of the status quo, of an Australian private sector looking to government for answers, not the entrepreneurial innovative Australia that will diversify the economy.

In a recent edition of The Australian financial adviser Stirling Larkin highlighted a major flaw in Australia’s reform strategy for competitiveness, noting:

“Australia led the way with the first of the two stages of globalisation during the 1980s when the requisite sacrifices were accepted. [It] then failed to embrace the second stage, which would have provided the promised benefits of the new paradigm. What this meant in practice, was that Australia withdrew from the manufacturing, industrial and heavier industries but then failed to draft any new plans to reallocate ingenuity and resources toward our distinctive competitive edges”.

The Innovation Plan calls for:

- a lower cost, business friendly environment with less regulation, lower taxes and more competitive markets;

- a more skilled labour force;

- better economic infrastructure; and

- industry policy that fosters innovation and entrepreneurship.

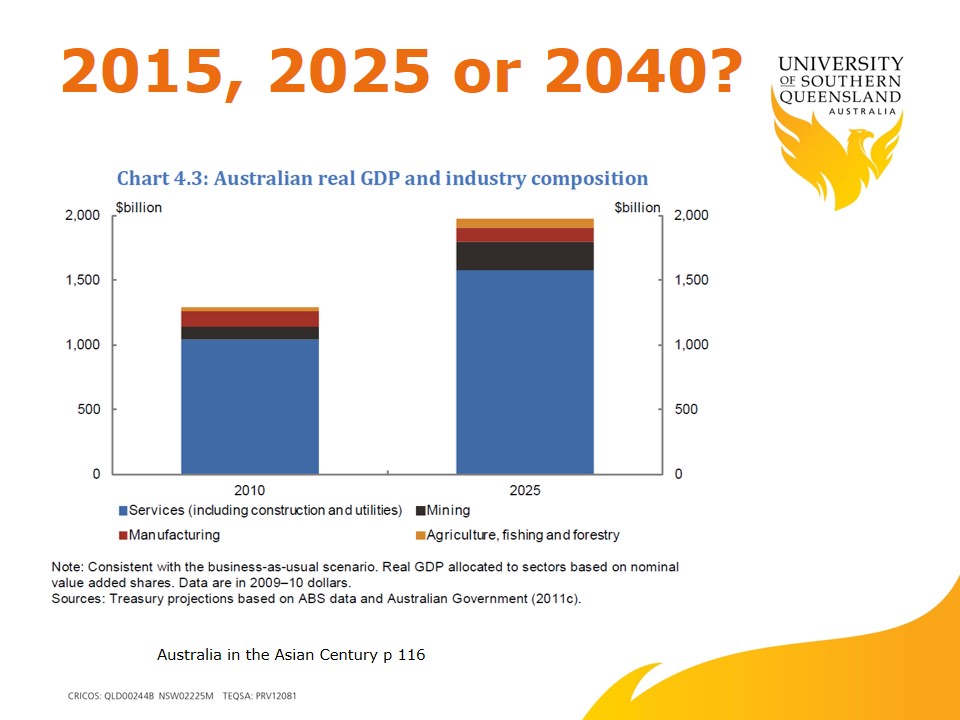

The current industry innovation plan is a plan for more of the same – as evidenced in this Treasury graph from Australia in the Asian Century which shows the relative proportions of the various sectors within the national economy being pretty much the same in 2025 as they are now.

Macfarlane’s plan courtesy of the Business Council of Australia is not a plan for entrepreneurs and does not emphasise achieving higher levels of entrepreneurship.

Where is the plan for removing the business growth barriers for young Australians? Holly Ransom the co-chair of the Y-20 in Australia will tell you that the growth rates of businesses owned by young people is something like 200% but 70% of these young entrepreneurs struggle to access capital.

Needed a focus on the entrepreneurial part of the economy

The heart of Australian business is those 54,000 mid-sized businesses with a turnover between $5 million and $250 million, 3% of all businesses, employing 24% of the workforce and generating 25% of gross value added. This is the group most likely to lead the diversification of our economy and set new directions within a policy framework encouraging innovation.

Instead right now Australia is dropping down the ladder in its ability to attract and retain high class talent. Australia now ranks 19 out of 60 countries in the World Talent Ranking, having slipped from No 5 position over the past decade.

Treasury also obviously doesn’t think that the services component in Australia’s exports is going to change substantially any time soon, and yet it is one of the key opportunities of the next generation – and must be a point of development emphasis in our attempt at diversifying the economy.

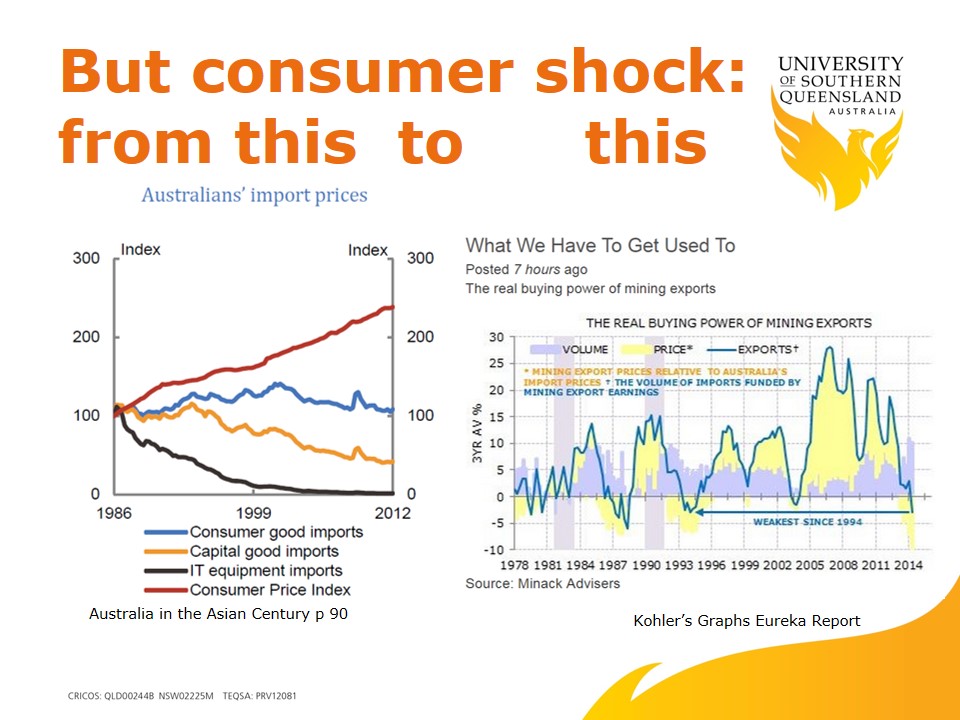

This is imperative if we are to avoid the shock of not being able to afford the imports that have come to characterise our homes, offices and lifestyles.

In the heyday of the resources boom with a strong Australian dollar, the cost of imports went down, CPI and wages went up, and Australians bought more and even had money left over for savings.

We are facing a very different scenario in the next half decade. Alan Kohler from The Eureka Report and ABC TV News showed quite graphically what happens to Australia when our commodities prices go through the floor – the volume of imports funded by mining exports also goes through the floor.

Kohler pointed out that by late 2014 the buying power of Australian mining exports was at its weakest since 1994 and it seems Reserve Bank Governor Glen Stevens sees an even lower exchange rate as necessary “to achieve balanced growth in the economy”.

Australia’s terms of trade has fallen 9% this year and 24% since hitting the high water mark in 2011. This has compounded greatly Joe Hockey’s challenge of balancing the budget anytime soon.

The Treasurer points to iron ore making up a fifth of our exports and its price having halved over 18 months – leaving with us what the commentators are calling a national ‘income recession’.

Witness the nature of an economy dependent on the commodity cycle. And the risks don’t stop with mineral exports. Energy also is increasingly volatile as a result of disruptive innovation.

Take LNG for example, with its long term contract prices pegged to the price of a barrel of oil.

In a world where oil prices were expected to go only one way – upwards, it seemed commercially smart to peg your LNG contract to oil.

But that arrangement took no account of the disruptive impacts of shale oil coming on to the market and making the US self sufficient again, the willingness of OPEC to drop its oil price to maintain volume, or the overall depressing effects of a turndown in demand in countries like China.

The upshot is that when oil gets down to US$80 a barrel LNG companies start to lose serious money on gas coming out of Gladstone.

In the last week of November the price of oil hit a low of US$67 a barrel, having dropped by 40% in three months.

In time, the hydrocarbons markets will catch up with the impacts of recent disruptive innovations and the markets will rationalise around the principles of supply and demand.

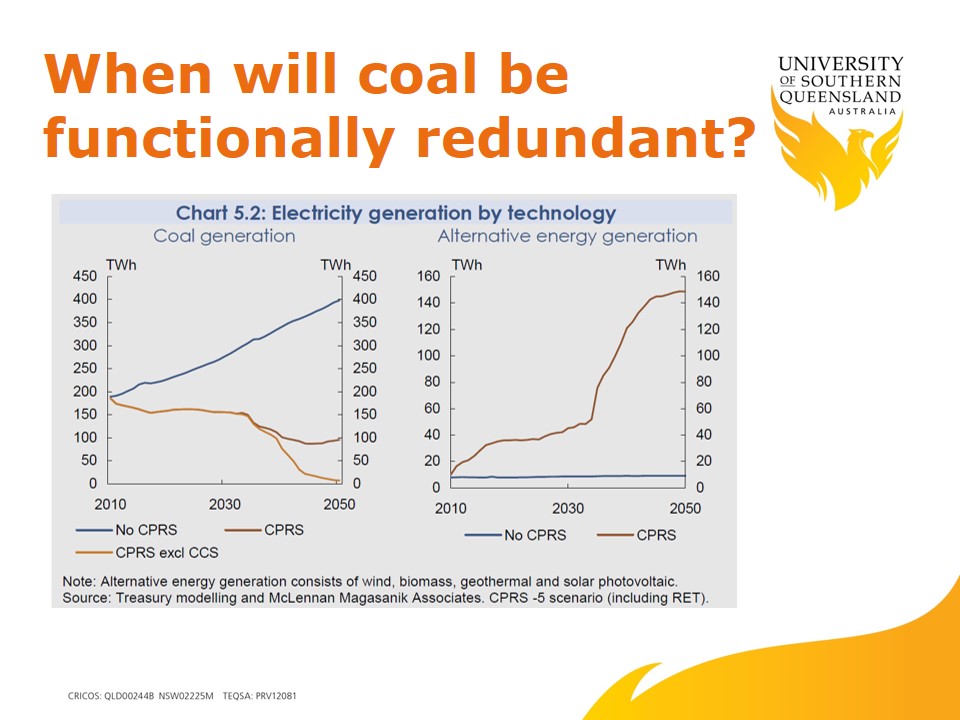

With thermal coal, however, barring some miracle happening with CO2 sequestration at power plants on an almost incomprehensible scale over two or three decades, the direction is a one way exit street.

Bluntly, Australia will reach the time when it will need to bite the bullet and exit thermal coal production.

Right now thermal coal is trying to slow down the inevitable by stripping costs out of its production to keep prices low – currently they are around $US60-70 a tonne. The current down cycle has seen about 200 million tonnes drop out of production globally.

And while this downturn should not be confused with the longer term superseding of coal as an energy source, increasingly major financial players like Citi investment bank question “whether coal will in fact play as significant a role as the coal industry may be suggesting in lifting developing nations out of energy poverty”.

Perhaps cognisant of the looming transition, Queensland Premier Campbell Newman says he wants Queenslanders “to find new ways of developing cleaner and greener fuels”. He promises a post-election $500 million will be taken from the leasing of State assets to underwrite R&D and commercialisation of cleaner energy technologies, especially those leveraging the State’s enormous investment in LNG.

In the years to 2040 thermal coal will be increasingly superseded first by gas, and thereafter increasingly by a mixture of next generation nuclear and renewables. We will exit the coal age long before we run out of coal, just as in eons past earlier generations did from the Stone Age.

Government interventions picking particular technologies to hasten the transition though come with their own risks. Look no further than the $200 million a year households without solar panels are paying to subsidise those with panels – the outcome of generous State Government feed in tariff payments to support the adoption of a form of renewable energy which these days can justify itself in savings and efficiency.

Possibly worse as an example of government chasing after an innovation that was already in the market was the Rudd/Gillard $500 million Green Car Innovation Fund.

Good government can fashion change without becoming a poor imitation of a venture capitalist.

If governments want to facilitate the transition to clean energy in most affordable fashion, there is nothing more efficient than removing subsidies on fossil fuel consumption and implementing an economy wide emissions trading scheme that puts a price on carbon.

Logic and the human will to survive suggests we will have one of those long before 2040.

Brand Australia: adapting our national image to be relevant tomorrow

Let me close out this presentation with a few observations on growth opportunities for Australia.

Tourism and international education are cornerstones to the human network that will shape our future. The more engaged the rest of the world is with us, the more options future Australians will enjoy.

To that end, the volume and variety of future visitors to Australia remains a vital conduit for global engagement with our country and its future.

This is how many of us still see ourselves, but does it engage with the rest of the world? It might be how we sell ourselves to ourselves – ie the brochure version of Australia – but it will take more than “spirit”, even good old fashioned “Aussie spirit” to take on the next 25 years.

Many Australians might console themselves with thoughts of their ‘exceptionalism’ and distance from all the problems of the wider world.

Some cling to a lingering vision of the Anglo Australia of the nineteenth and twentieth centuries and toast a ‘Brand Australia’ that embodies muscular, stoic, resilient values.

But how relevant will that image be in building on, say for example, the current $15.74 billion international student industry – made up of 388,000 students drawn largely of China, India and Pakistan – who spent $5.3 billion on university tuition fees last year?

How will the brochure view of Australia help us against stiffening competition from Canada, the US and Britain as destinations for students?

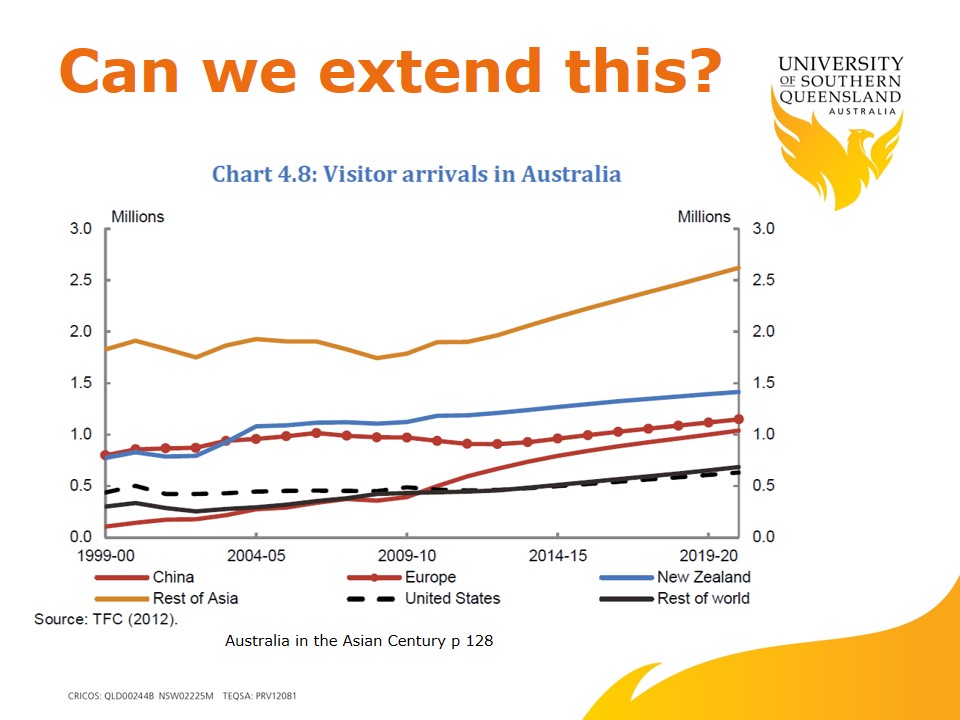

Encouragingly, future projections point upwards in all source countries for visitors to Australia – with the strongest growth from China and the rest of Asia. Phil Ruthven from IBIS thinks tourism exports could overtake the value our mining exports by the early 2030s.

Amidst the increasingly complex and varied human engagement between Australia and the rest of the world, sometime along the way our sense of selves is also likely to change.

Growth opportunities

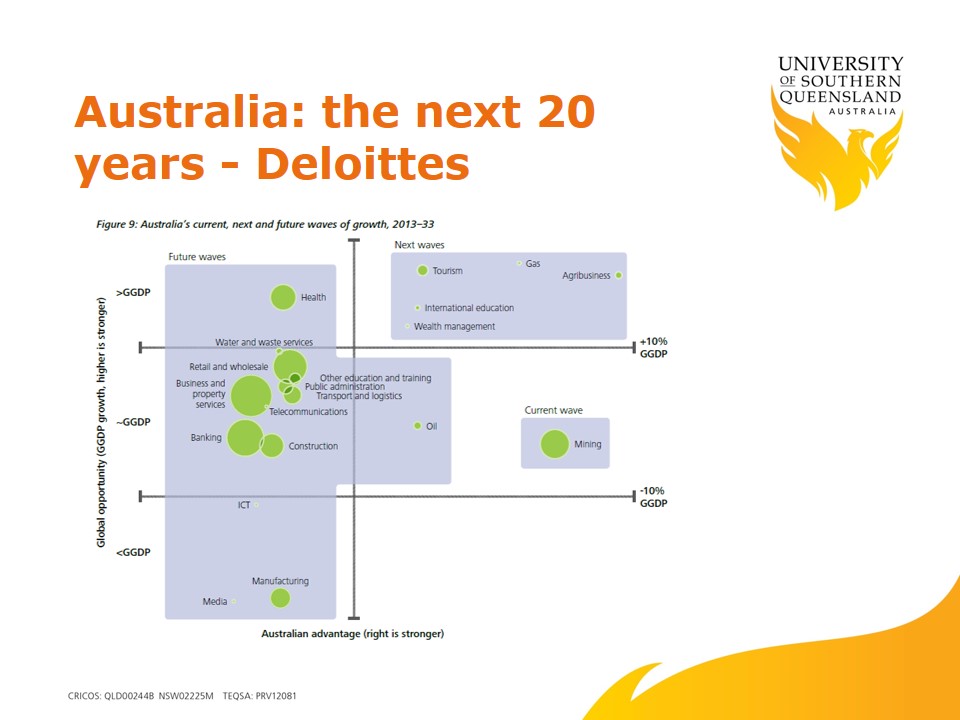

By now you will have heard of the Deloitte Growth25, the top 25 growth opportunities for Australia in the years ahead, anticipating new waves and a re-mixing of our economic output.

While mining might be top of the pops right now, Deloitte predict that its ‘Fantastic Five’ – agribusiness, gas, tourism, international education, and curiously, wealth management will shape the Australian economy into the future. These sectors are expected to be the stars but they also identify 19 other sectors which are expected to feature strongly – everything from ICT to parcel delivery.

While there has been much discussion around the sectors and their rankings, less evident I believe is the vital qualifier attached by Deloitte which suggests that their predictions will only happen if Australia resolves itself into a growth compact.

The 8 point Deloitte growth resolution requires everyone to lift their game – from politicians and their cheap political points scoring, to governments being robust and efficient in their policy development and program delivery, to workforce composition, gender equity, and long term thinking in business – it all adds up to a much sharper, smarter more collaborative approach – a genuine non-political Team Australia path to take.

Is government in Australia up to the job?

The Deloitte check-list on what has to change for Australia to be competitive into the future leads inevitably and in conclusion to the question: Is our system of government up to the challenge?

While government is a necessary public good, it should only be involved in things people cannot do for themselves.

For that reason Australians should be concerned at the creeping encroachment of government into many non-essential aspects of our lives and conversely we should take a hard close look at our own expectations in what is expected of government.

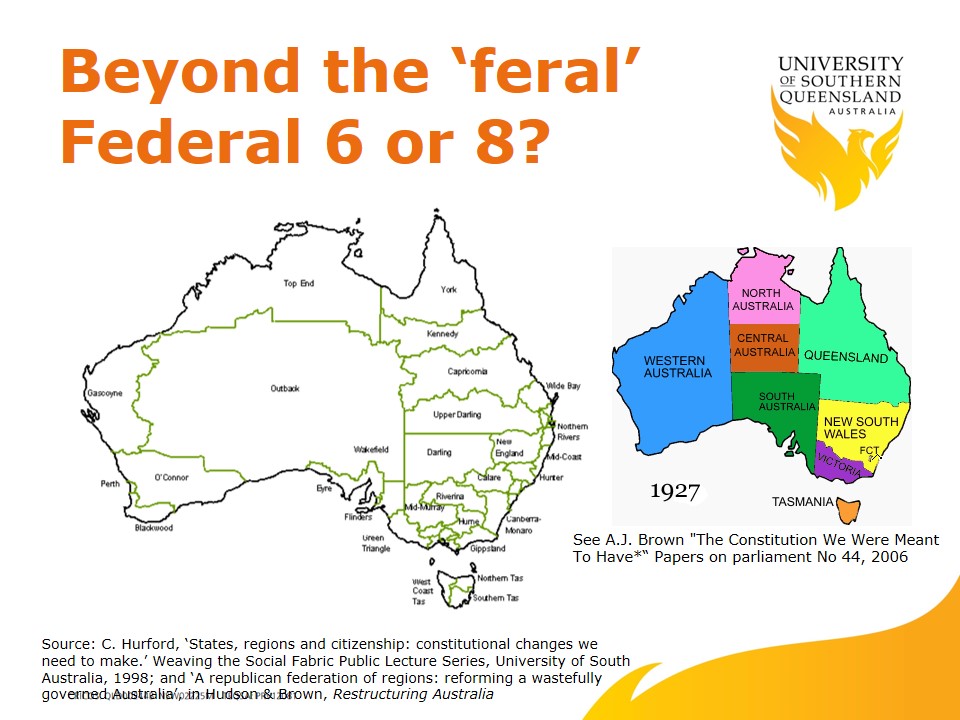

Recently the Committee for the Economic Development of Australia (CEDA) released its major research report into federalism in Australia and suggested among other things that the federal arrangement be overhauled.

My personal list of subjects (and many of these are addressed in the CEDA report) that should be on the national discussion table includes:

- Establishment of a Decennial Constitutional Convention

- Restoration of core functions like education and health to the State

- Active implementation of the principle of Subsidiarity

- General application of User pays for many infrastructural and commons service

- Hypothecation of regulatory fees and charges to specific purpose

- New States in northern Australia

- Active promotion of the concepts of self –organisation and self- determination across Australia

- Reform of the context of local government within the States

What we have to achieve is a restoration of the sovereignty of the States and an equivalent capacity for them to raise revenue and deal constructively with local government by adhering to the principles of subsidiarity.

Even the idea of new states is not original. Professor Geoffrey Blainey has championed the idea for years and Chris Hurford a former Minister in the Hawke Government came up with a model of regional government which aligns with many of the current crop of RDAs.

From 1926 until 1931 the current Northern Territory was divided into two provinces with what turned out to be a temporary creation of the Central Australia Territory based on Alice Springs.

For those of you in local government, constitutional recognition of local government will do nothing to materially improve the financial and resourcing capacity of your sector. The real challenge is achieving some strategic and organisational alignment between the Commonwealth and the States that is valid constitutionally, culturally and politically.

Speaking at Tenterfield in late October 2014 for the 125th Anniversary of the Sir Henry Parkes Oration, Prime Minister Tony Abbott gave a less than rousing invitation to reform of the federation.

He said:

“Going forward we need to think more flexibly about our constitutional and government bases, evincing a willingness to update and make relevant the public institutions through which we aim to achieve collective common goods”.

“The problem, then, was to create a nation from six colonies. The problem now, is to create a more rational system of government for the nation that we undoubtedly have become….. It’s to realise, if possible, the self-evident benefits of less waste, less overlap, less duplication; it’s to end the blame game by trying to ensure that voters know who’s really responsible for the things they don’t like; and it’s to harvest the multi-billion dollar benefits in better services and lower costs that would come from successful reform”.

Personally, I would have liked more vision and a stronger more inspiring statement of what we as a nation should be aiming to achieve in the years ahead and why a reformed Federation was so important for that to that mission.

Maybe the Prime Minister was in tune with his constituency. Maybe that is what we as Australians are focused on: dollars and entitlements and services

Abbott’s speech was by no means inspiration nor visionary for the nation – emphasising more the accountabilities of an account manager or efficiency auditor.

Looking to the future, the capacity and efficiency of our system of government as well as political vision will be crucial if the country is to create opportunities for itself.

We will need entrepreneurs and tinkerers and curious smart people working at the edge in the world of the “anti-fragile”, making mistakes, quickly recovering and then launching on to something potentially disruptive in its significance.

That’s how we will make the “anti-fragile” Australia of 2040 – a nation up to the challenges and opportunities of a vastly different world and the promise of generations still in the forming

We need people who will question consensus and see projections and extrapolations for what they are – leaps into the unknown in an imperfect non-rational world

What we don’t need is more ‘directed research’ or state/corporate investment in trying to achieve the “future breakthrough” – call it picking winners.

Most of all we need leaders and teachers who are going to help young people believe that their goals are achievable and that education, creativity and hard work will pay off.

Thank you.